+380 67 625 91 65

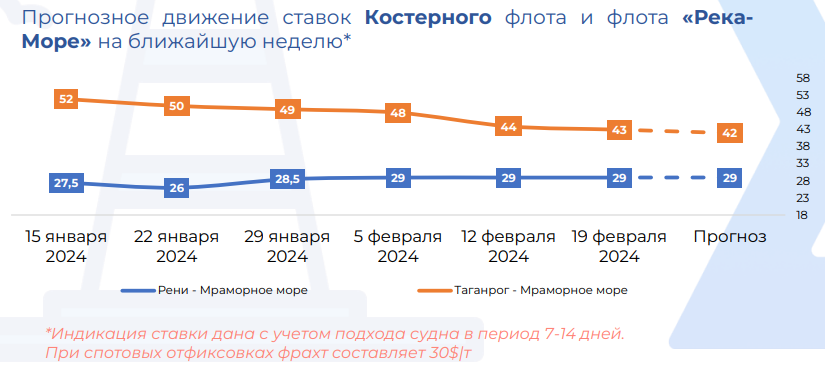

+380 67 625 91 65On the Black Sea market, current activity remains at a low level, despite an increase in available vessels this week. The main cargo flow continues to come from Russia and Ukraine. There is a desire among most Charterers to reduce rates, while shipowners are successfully resisting, keeping them at a stable level.

Cargo traffic from Ukraine and Russia is mainly focused on grains and coal to Mediterranean countries and Egypt. Recently, deals have been concluded for wheat and corn from Izmail and Reni to Egypt, as well as barley from Izmail to Tunisia. However, there is little sign of increased activity in the region in the coming weeks. Demand for grain remains almost unchanged, and lower prices for wheat and maize exports are affecting logistics costs. Shipowners are keen to maintain current rates in conditions of stable tonnage supply and a lack of demand growth.

The Mediterranean market is also experiencing low activity due to a surplus of available vessels and limited cargoes. This leads to increased competition for available cargoes, complicating the position of shipowners. Some recovery is seen in the fertilizer segment, with deals for urea shipments from Egypt to Sicily and Greece, as well as salt shipments from Egypt to Adriatic ports. There are also deals for steel shipments from Alexandria to Limassol and other cargoes from Marmara ports to Romania and Bulgaria.

In the Sea of Azov, the grain and coal trade continues to be slow, putting pressure on freight rates. Shipowners are trying to slow down the rates to stabilize them at current levels, amid limited demand for Russian grain and coal, especially in Turkey. Activity is mainly focused on grain shipments from Rostov and Azov towards Marmara. However, there are no clear signs of increased activity and improved rates in the region at present.