+380 67 625 91 65

+380 67 625 91 65The Black Sea freight market has faced a number of significant challenges in recent weeks. Eid al-Adha holidays, Turkey’s ban on wheat import and excessive tonnage create difficult conditions for shipowners. Spot market remains sluggish. Shipowners and brokers are hoping for the start of the new grain season, which should increase activity. However, the excess of vessels from the Azov Sea aggravates the situation on the Black Sea and Marmara Sea markets. Freight rates remain at minimum levels. For example, rates for the transportation of 6-7 thousand tons of corn or soybeans from Izmail to the Mediterranean are $18–19 per ton. At the same time, owners of old Arabian vessels are trying to get at least $21-22 per ton. The outlook for the Black Sea freight market remains gloomy.

The Mediterranean freight market has also faced serious challenges in recent weeks. The main problem is excessive tonnage, which leads to high competition among shipowners and lower freight rates. Eid al-Fitr holidays also reduced activity, which led to further decrease in demand for transportation. Freight rates for major cargoes such as grain and coal continue to decline. Demand for transportation is low and cargo volumes are insufficient to maintain stable rates. Shipowners are forced to make significant concessions to get orders. The outlook for the Mediterranean freight market remains disappointing. Excess tonnage and lack of cargoes will continue to put pressure on freight rates.

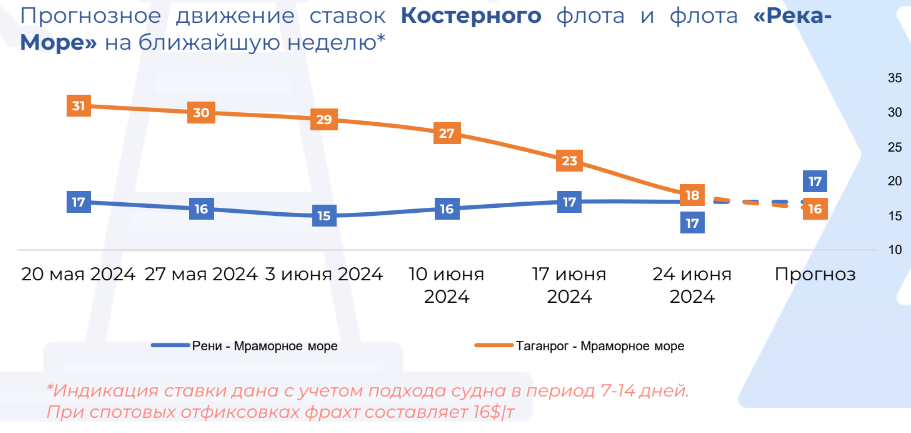

The Azov Sea freight market is also under significant pressure. Turkey’s ban on wheat imports, which came into effect on June 21, had a significant impact on the market, as Turkey was the main consumer of Russian grain from the Azov region. As a result, transportation volumes decreased, which led to a drop in freight rates. Excess tonnage increases pressure on the market. The large number of available vessels leads to high competition among shipowners, which forces them to reduce rates to get orders. Many shipowners are looking for alternative routes and cargoes, but opportunities are limited.

The forecast for the Azov Sea freight market remains gloomy. Even expected growth of exported grain volumes at the end of June – beginning of July may lead to only slight increase of rates, about $3-4 per ton, which will only allow to reach the level of operating expenses.