+380 67 625 91 65

+380 67 625 91 65The Black Sea continues to be a region that faces serious challenges for shipowners. Despite some activity in the market, the volume of firm offers for grain cargoes remains very limited. This creates significant pressure on freight rates and prevents their noticeable growth. Attempts by shipowners to raise rates are met with resistance from exporters, who are not ready to pay more due to low prices for wheat and corn in key importing countries. As a result, many vessels remain idle, intensifying competition for each cargo. Additional pressure on the market is exerted by rising fuel prices, forcing shipowners to reduce their demands. The market is likely to remain tight in the coming weeks, and freight rates will continue to be under pressure.

In the Mediterranean, the situation also remains challenging due to the imbalance between tonnage supply and demand. There was a slight improvement in fertilizer shipments from North African ports, but this was not enough to compensate for the overall cargo deficit. Shipowners are trying to keep rates steady, but their ability to do so is limited by high fuel costs and an excessive number of available vessels. Additional difficulties are created by low demand for construction materials and metallurgical products, which worsens the market situation. In such conditions, owners are forced to look for new ways to optimize operations and reduce costs. In the short term, the Mediterranean market is likely to remain under pressure, although the fertilizer transportation segment may show slight growth.

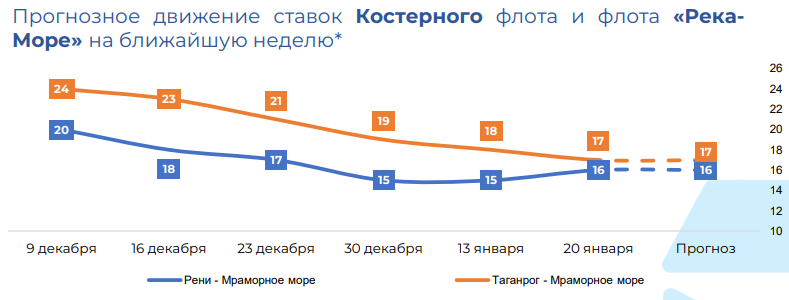

Low activity on the freight market remains in the Sea of Azov. Grain and coal exports from Russian ports practically did not grow even after the holiday period ended, which supports stagnation. Shipowners’ attempts to raise rates are faced with exporters’ reluctance to increase expenses, limiting themselves to the minimum possible amounts. Long voyages provide higher income but remain rare in current conditions. High competition among shipowners increases pressure on rates, forcing them to find new ways to adapt to market realities. In the coming months, the market is likely to maintain difficult dynamics, but increased export volumes may lead to partial stabilization.